Why you need trauma cover

Infographic-trauma-cover-01

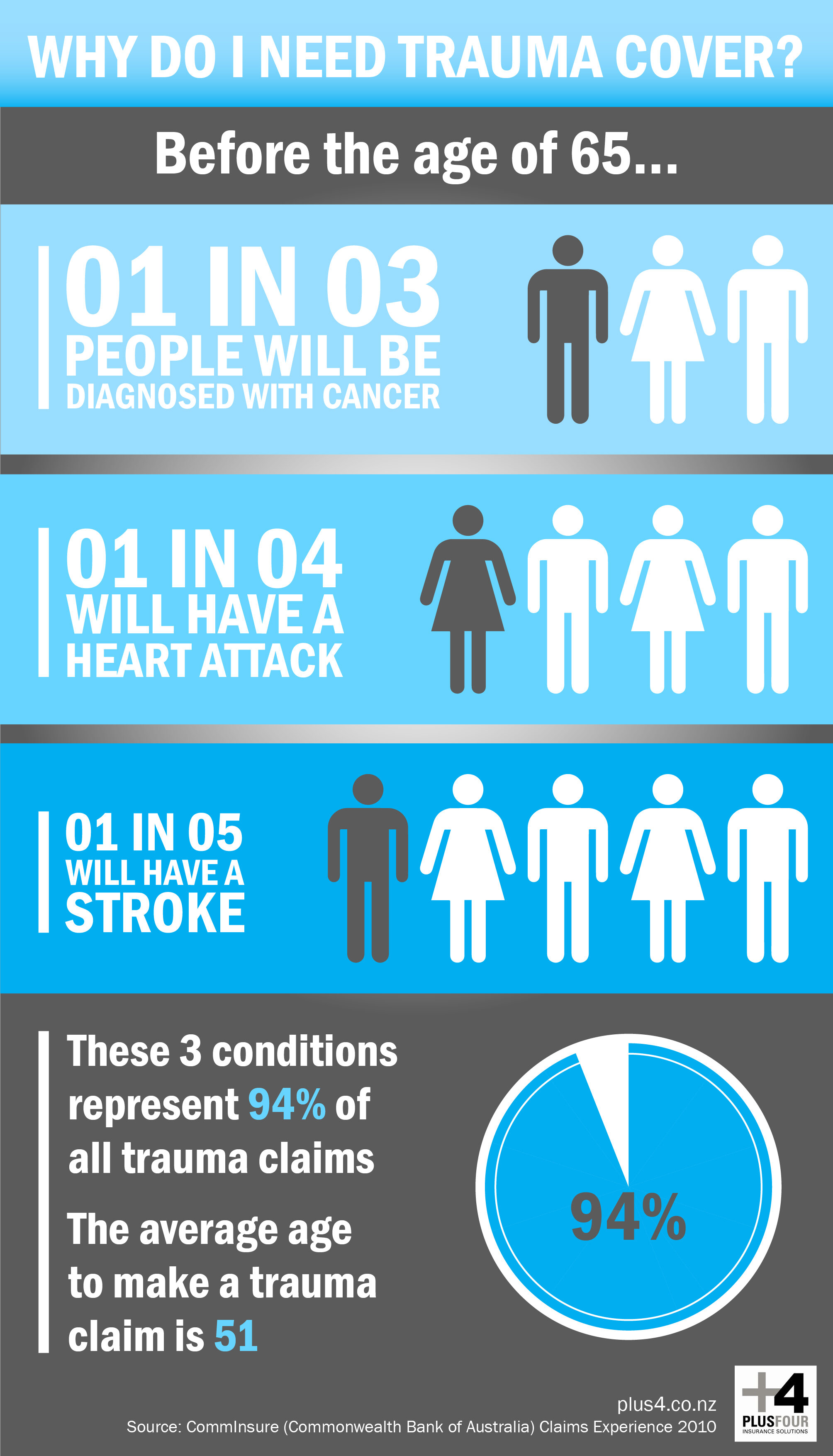

Trauma protection is an important part of your insurance coverage, but we often find it is poorly understood by clients. Trauma protection is a personal cover providing a lump sum payment in the event of a diagnosis of certain illnesses or if you experience specified injuries. Different providers have slightly different lists of illnesses or injuries, but all include cancer, heart attack and stroke. Injuries can include head trauma, burns or time spent in intensive care. The infographic below shows the most common claims on trauma covers.

How do you know if trauma protection is right for you?

If you have medical cover and income protection, having trauma protection can feel like doubling up, but there are a few reasons it can be worth having trauma cover as well, or why it may actually be your best option. One of the benefits of trauma protection is you can use the lump sum pay out however you see fit – such as reducing debt, covering living expenses, paying for alternative treatments or a holiday to recuperate. While income protection is important to have, it only covers the insured person if they are unable to work. Some of the challenges life can throw at our families mean that we want or need to have time off work to be there to help our loved ones. Many trauma policies also cover children - this means that if a child suffers one of the included injuries or illnesses the parents can take time from work to be with the family and focus on recovery without worrying about bills. Someone who isn’t in paid work, such as a family caregiver, can get trauma cover – meaning should something happen to them, their spouse can take time off work to be with them and focus on recovery and not have to worry about bills. Some people, such as those in dangerous work, can struggle to get income protection which means trauma cover is the best option. Likewise, if income protection is out of your budget trauma is the next best.

How much is trauma cover, and how much should I get?

Determining how much trauma cover to get, or which provider’s policy is best for you, can be challenging, which is why it is always best to talk to an adviser, who can take into account your individual circumstances, your budget, other cover you have in place and your lifestyle. Unless you include a “buy back” in your premium, once you have used your trauma cover it is gone. The buy back rate is usually very small (as low as $4 a month) but on some policies it can allow you to claim up to five times, provided there is at least six months between claims and the claim is for a separate event. While it may sound unlikely to claim more than once, it is not uncommon for people to claim three times on one policy. If you think trauma cover is something you need to consider as part of your personal cover plan, get in touch with one of our advisers today.